As of close of business on December 20, 2024, Tortoise Energy Independence Fund, Inc. (NDP) has merged into the Tortoise Power and Energy Infrastructure Fund. Effective 3/24/25 Tortoise Power and Energy Infrastructure Fund changed it's name to Tortoise Essential Energy Fund (TPZ). Distribution and tax information is provided for informational purposes.

NDP Distribution Summary

See complete history Hide complete history| Declared | Record Date | Payment Date | Amount | Market Price | NAV | DRIP 1 | |||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 11/25/2024 | 12/06/2024 | 12/13/2024 | 0.2550 | 41.68 | 42.09 | 41.1512 | |||||||

| 11/04/2024 | 11/22/2024 | 11/29/2024 | 0.6300 | 44.10 | 45.10 | 43.5280 | |||||||

| 08/08/2024 | 08/23/2024 | 08/30/2024 | 0.6300 | 38.23 | 39.90 | 37.8502 | |||||||

| 05/08/2024 | 05/24/2024 | 05/31/2024 | 0.6300 | 33.98 | 39.70 | 33.5555 | |||||||

| 02/07/2024 | 02/22/2024 | 02/29/2024 | 0.6300 | 30.81 | 35.87 | 31.3046 | |||||||

| Fiscal Year 2024 Total: | $2.7750 | ||||||||||||

| Fiscal Year 2024 Total: $2.78 | |||||||||||||

| 11/09/2023 | 11/22/2023 | 11/30/2023 | 0.6300 | 28.95 | 35.45 | 28.9193 | |||||||

| 8/10/2023 | 8/24/2023 | 8/31/2023 | 0.6300 | 31.15 | 36.27 | 31.9195 | |||||||

| 5/09/2023 | 5/24/2023 | 5/31/2023 | 0.6300 | 27.08 | 31.53 | 27.4977 | |||||||

| 2/09/2023 | 2/21/2023 | 2/28/2023 | 0.6300 | 29.46 | 33.86 | 30.1007 | |||||||

| Fiscal Year 2023 Total: | $2.5200 | ||||||||||||

| Fiscal Year 2023 Total: $2.52 | |||||||||||||

| 11/08/2022 | 11/23/2022 | 11/30/2022 | 0.5600 | 31.41 | 38.25 | 31.952781 | |||||||

| 8/09/2022 | 8/24/2022 | 8/31/2022 | 0.5600 | 32.37 | 36.77 | 31.398775 | |||||||

| 5/10/2022 | 5/24/2022 | 5/31/2022 | 0.4800 | 32.47 | 38.69 | 33.694752 | |||||||

| 1/18/2022 | 2/21/2022 | 2/28/2022 | 0.4800 | 27.59 | 31.76 | 27.974173 | |||||||

| Fiscal Year 2022 Total: | $2.0800 | ||||||||||||

| Fiscal Year 2022 Total: $2.08 | |||||||||||||

| 11/9/2021 | 11/23/2021 | 11/30/2021 | 0.310 | 22.24 | 25.13 | 22.291919 | |||||||

| 8/9/2021 | 8/24/2021 | 8/31/2021 | 0.310 | 19.49 | 22.00 | 19.577222 | |||||||

| Fiscal Year 2021 Total: | $0.620 | ||||||||||||

| Fiscal Year 2021 Total: $0.62 | |||||||||||||

| 02/12/2020 | 02/21/2020 | 02/28/2020 | 0.1000 | 2.72 | 3.04 | 2.675420 | |||||||

| Fiscal Year 2020 Total: | $0.1000 | ||||||||||||

| Fiscal Year 2020 Total: $0.10 | |||||||||||||

| 11/04/2019 | 11/22/2019 | 11/29/2019 | 0.1000 | 3.63 | 4.17 | 3.68 | |||||||

| 8/8/2019 | 8/23/2019 | 8/30/2019 | 0.1000 | 3.99 | 4.42 | 4.08 | |||||||

| 5/6/2019 | 5/24/2019 | 5/31/2019 | 0.4375 | 7.40 | 5.94 | 7.03 | |||||||

| 2/5/2019 | 2/21/2019 | 2/28/2019 | 0.4375 | 8.08 | 7.57 | 7.68 | |||||||

| Fiscal Year 2019 Total: | $1.0750 | ||||||||||||

| Fiscal Year 2019 Total: $1.08 | |||||||||||||

| 02/08/2018 | 02/21/2018 | 02/28/2018 | 0.4375 | 11.80 | 11.38 | 11.38 | |||||||

| 05/04/2018 | 05/24/2018 | 05/31/2018 | 0.4375 | 12.47 | 12.18 | 12.06 | |||||||

| 08/06/2018 | 08/24/2018 | 08/31/2018 | 0.4375 | 12.69 | 11.76 | 12.06 | |||||||

| 11/05/2018 | 11/23/2018 | 11/30/2018 | 0.4375 | 9.00 | 9.02 | 9.02 | |||||||

| Fiscal Year 2018 Total: | $1.7500 | ||||||||||||

| Fiscal Year 2018 Total: $1.75 | |||||||||||||

| 02/10/2017 | 02/21/2017 | 02/28/2017 | 0.4375 | 16.33 | 15.84 | 15.84 | |||||||

| 05/08/2017 | 05/24/2017 | 05/31/2017 | 0.4375 | 14.43 | 13.63 | 13.71 | |||||||

| 08/07/2017 | 08/24/2017 | 08/31/2017 | 0.4375 | 12.61 | 11.79 | 11.98 | |||||||

| 11/06/2017 | 11/22/2017 | 11/30/2017 | 0.4375 | 12.39 | 12.88 | 12.35 | |||||||

| Fiscal Year 2017 Total: | $1.7500 | ||||||||||||

| Fiscal Year 2017 Total: $1.75 | |||||||||||||

| 02/09/2016 | 02/22/2016 | 02/29/2016 | 0.4375 | 9.76 | 11.35 | 10.56 | |||||||

| 05/10/2016 | 05/24/2016 | 05/31/2016 | 0.4375 | 13.71 | 15.30 | 14.21 | |||||||

| 08/08/2016 | 08/24/2016 | 08/31/2016 | 0.4375 | 15.61 | 16.22 | 15.97 | |||||||

| 11/07/2016 | 11/23/2016 | 11/30/2016 | 0.4375 | 15.85 | 16.95 | 15.96 | |||||||

| Fiscal Year 2016 Total: | $1.7500 | ||||||||||||

| Fiscal Year 2016 Total: $1.75 | |||||||||||||

| 02/09/2015 | 02/20/2015 | 02/27/2015 | 0.4375 | 21.25 | 22.12 | 21.36 | |||||||

| 05/11/2015 | 05/22/2015 | 05/29/2015 | 0.4375 | 19.47 | 21.61 | 19.40 | |||||||

| 08/12/2015 | 08/24/2015 | 08/31/2015 | 0.4375 | 14.64 | 16.65 | 14.33 | |||||||

| 11/09/2015 | 11/23/2015 | 11/30/2015 | 0.4375 | 13.18 | 15.53 | 12.23 | |||||||

| Fiscal Year 2015 Total: | $1.7500 | ||||||||||||

| Fiscal Year 2015 Total: $1.75 | |||||||||||||

| 02/10/2014 | 02/21/2014 | 02/28/2014 | 0.4375 | 24.61 | 27.70 | 24.69 | |||||||

| 05/12/2014 | 05/22/2014 | 05/30/2014 | 0.4375 | 26.78 | 30.38 | 26.98 | |||||||

| 08/08/2014 | 08/22/2014 | 08/29/2014 | 0.4375 | 27.32 | 31.04 | 26.76 | |||||||

| 11/10/2014 | 11/21/2014 | 11/28/2014 | 0.4375 | 21.29 | 22.76 | 21.35 | |||||||

| Fiscal Year 2014 Total: | $1.7500 | ||||||||||||

| Fiscal Year 2014 Total: $1.75 | |||||||||||||

| 02/11/2013 | 02/21/2013 | 03/01/2013 | 0.4375 | 24.02 | 24.11 | 24.11 | |||||||

| 05/06/2013 | 05/23/2013 | 06/03/2013 | 0.4375 | 24.91 | 24.65 | 24.65 | |||||||

| 08/08/2013 | 08/23/2013 | 09/03/2013 | 0.4375 | 23.98 | 25.82 | 24.39 | |||||||

| 11/11/2013 | 11/22/2013 | 11/29/2013 | 0.4375 | 24.08 | 26.49 | 23.85 | |||||||

| Fiscal Year 2013 Total: | $1.7500 | ||||||||||||

| Fiscal Year 2013 Total: $1.75 | |||||||||||||

| 09/05/2012 | 11/23/2012 | 11/30/2012 | 0.4375 | 22.33 | 22.73 | 21.85 | |||||||

| Fiscal Year 2012 Total: | $0.4375 | ||||||||||||

| Fiscal Year 2012 Total: $0.44 | |||||||||||||

-

Price of shares issued pursuant to company-sponsored dividend reimbursement plan. Amounts are rounded to the nearest whole cent.

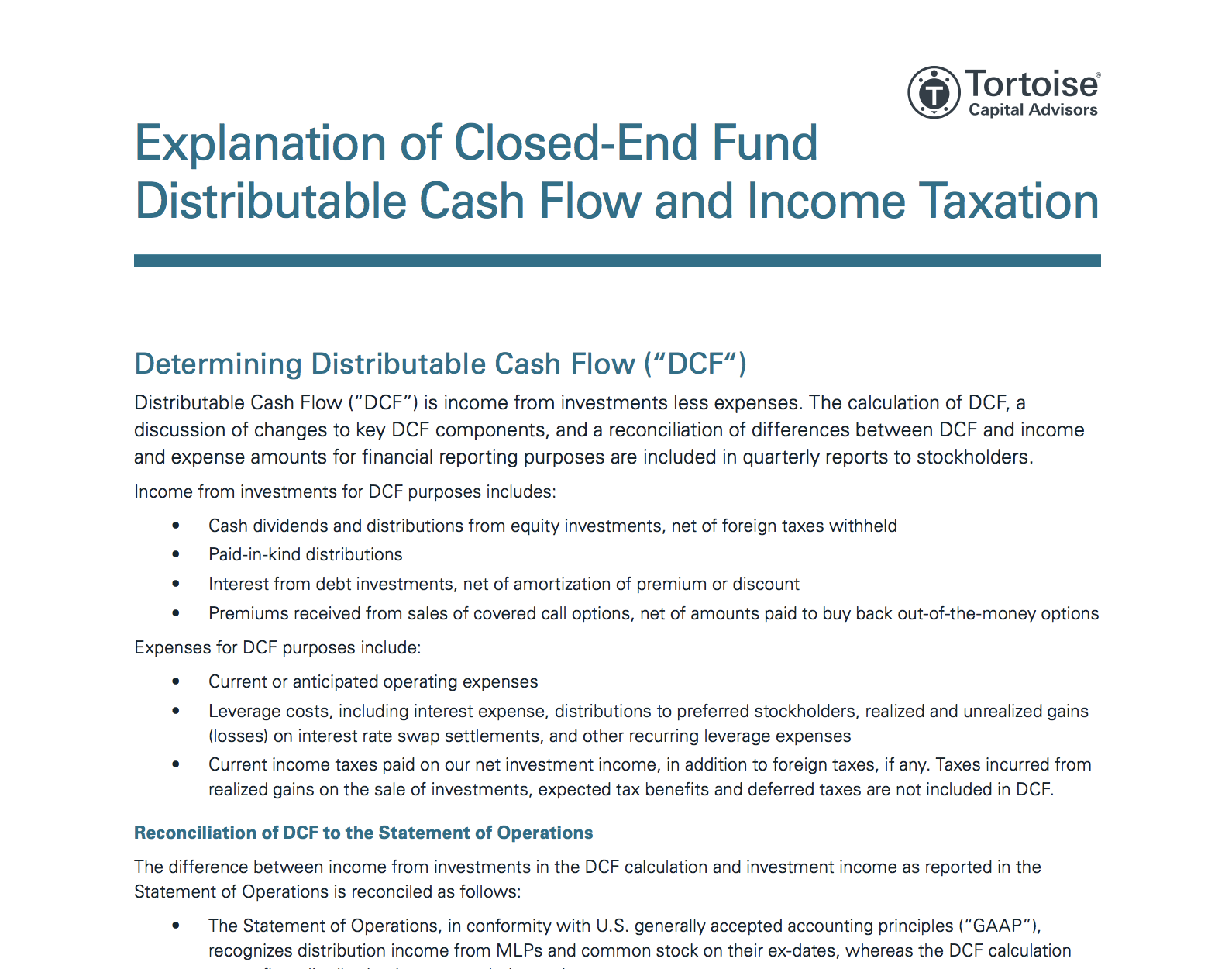

Determining distributions to stockholders

The fund has adopted a managed distribution policy (“MDP”). Annual distribution amounts are expected to fall in the range of 7% to 10% of the average week-ending net asset value (“NAV”) per share for the prior fiscal semi-annual period. Distribution amounts will be reset both up and down to provide a consistent return on trailing NAV. Under the MDP, distribution amounts will normally be reset in February and August, with no changes in distribution amounts in May and November. The fund may designate a portion of its distributions as capital gains and may also distribute additional capital gains in the last quarter of the year to meet annual excise distribution requirements. Distribution amounts are subject to change from time to time at the discretion of the Board.

For more details, see NDP's complete distribution and tax information here.

Tax Information (NYSE: NDP) Tortoise Energy Independence Fund, Inc

Find distributions and other tax-related resources for Tortoise Capital closed-end funds. Tax forms, publications and instructions are available for download from the IRS Web site.

Annual 1099-DIV

2024 Common Stock Tax Information

| Total Distributions Per Share | Total Ordinary Dividends Box 1a 1 | Qualified Dividends Box 1b 2 | Capital Gain Distributions Box 2a 3 | Nondividend Distributions Box 3 4 |

|---|---|---|---|---|

| $2.7750 | $0.4268 | $0.4268 | $0.0000 | $2.3482 |

| Total 2024 Distributions: | $0.4268 | $0.4268 | $0.0000 | $2.3482 |

-

Box 1a: Ordinary dividends are taxed at ordinary income tax rates.

-

Box 1b: Qualified dividends are taxed at capital gain tax rates if the stockholder meets holding period requirements.

-

Box 2a: Capital gain distributions (long-term) are taxed at capital gain tax rates.

-

Box 3: Nondividend distributions are nontaxable and considered return of capital.

For stockholders who participated in the company-sponsored dividend reinvestment plan, the tax basis of shares acquired is the greater of the purchase price or the market close price on the payment date.

Nothing contained herein should be construed as tax advice; consult your tax adviser for more information. Furthermore, you may not rely upon any information herein for the purpose of avoiding any penalties that may be imposed under the Internal Revenue Code.

Report of Organizational Actions Affecting Basis of Securities

Effective January 1, 2012, issuers of regulated investment company securities must complete Form 8937 to report organizational actions, including nontaxable distributions, that affect the basis of the securities involved in the organizational action. The information contained below is intended to satisfy the requirements of public reporting under section 1.6045B-1(a)(3) and (b)(4) of the Treasury Regulations.

Annual 1099-DIV

2023 Common Stock Tax Information

| Total Distributions Per Share | Total Ordinary Dividends Box 1a 1 | Qualified Dividends Box 1b 2 | Capital Gain Distributions Box 2a 3 | Nondividend Distributions Box 3 4 |

|---|---|---|---|---|

| $2.5200 | $0.7469 | $0.7469 | $0.0000 | $1.7731 |

| Total 2023 Distributions: | $0.7469 | $0.7469 | $0.0000 | $1.7731 |

-

Box 1a: Ordinary dividends are taxed at ordinary income tax rates.

-

Box 1b: Qualified dividends are taxed at capital gain tax rates if the stockholder meets holding period requirements.

-

Box 2a: Capital gain distributions (long-term) are taxed at capital gain tax rates.

-

Box 3: Nondividend distributions are nontaxable and considered return of capital.

For stockholders who participated in the company sponsored dividend reinvestment plan, the tax basis of shares acquired is the greater of the purchase price or the market close price on the payment date.

Report of Organizational Actions Affecting Basis of Securities

Effective January 1, 2012, issuers of regulated investment company securities must complete Form 8937 to report organizational actions, including nontaxable distributions, that affect the basis of the securities involved in the organizational action. The information contained below is intended to satisfy the requirements of public reporting under section 1.6045B-1(a)(3) and (b)(4) of the Treasury Regulations.

Nothing contained herein should be construed as tax advice; consult your tax adviser for more information. Furthermore, you may not rely upon any information herein for the purpose of avoiding any penalties that may be imposed under the Internal Revenue Code.

Annual 1099-DIV

2022 Common Stock Tax Information

| Total Distributions Per Share | Total Ordinary Dividends Box 1a 1 | Qualified Dividends Box 1b 2 | Capital Gain Distributions Box 2a 3 | Nondividend Distributions Box 3 4 |

|---|---|---|---|---|

| $2.0800 | $0.8219 | $0.8219 | $0.0000 | $1.2581 |

| Total 2022 Distributions: | $0.8219 | $0.8219 | $0.0000 |

-

Box 1a: Ordinary dividends are taxed at ordinary income tax rates.

-

Box 1b: Qualified dividends are taxed at capital gain tax rates if the stockholder meets holding period requirements.

-

Box 2a: Capital gain distributions (long-term) are taxed at capital gain tax rates.

-

Box 3: Nondividend distributions are nontaxable and considered return of capital.

For stockholders who participated in the company sponsored dividend reinvestment plan, the tax basis of shares acquired is the greater of the purchase price or the market close price on the payment date.

Report of Organizational Actions Affecting Basis of Securities

Effective January 1, 2012, issuers of regulated investment company securities must complete Form 8937 to report organizational actions, including nontaxable distributions, that affect the basis of the securities involved in the organizational action. The information contained below is intended to satisfy the requirements of public reporting under section 1.6045B-1(a)(3) and (b)(4) of the Treasury Regulations.

Nothing contained herein should be construed as tax advice; consult your tax adviser for more information. Furthermore, you may not rely upon any information herein for the purpose of avoiding any penalties that may be imposed under the Internal Revenue Code.

Annual 1099-DIV

2021 Common Stock Tax Information

| Total Distributions Per Share | Total Ordinary Dividends Box 1a 1 | Qualified Dividends Box 1b 2 | Capital Gain Distributions Box 2a 3 | Nondividend Distributions Box 3 4 |

|---|---|---|---|---|

| $0.310000 | $0.023300 | $0.023300 | $0.000000 | $0.286700 |

| Total 2021 Distributions: | $0.023300 | $0.023300 | $0.000000 | $0.286700 |

-

Box 1a: Ordinary dividends are taxed at ordinary income tax rates.

-

Box 1b: Qualified dividends are taxed at capital gain tax rates if the stockholder meets holding period requirements.

-

Box 2a: Capital gain distributions (long-term) are taxed at capital gain tax rates.

-

Box 3: Nondividend distributions are nontaxable and considered return of capital.

For stockholders who participated in the company sponsored dividend reinvestment plan, the tax basis of shares acquired is the greater of the purchase price or the market close price on the payment date.

Report of Organizational Actions Affecting Basis of Securities

Effective January 1, 2012, issuers of regulated investment company securities must complete Form 8937 to report organizational actions, including nontaxable distributions, that affect the basis of the securities involved in the organizational action. The information contained below is intended to satisfy the requirements of public reporting under section 1.6045B-1(a)(3) and (b)(4) of the Treasury Regulations.

Nothing contained herein should be construed as tax advice; consult your tax adviser for more information. Furthermore, you may not rely upon any information herein for the purpose of avoiding any penalties that may be imposed under the Internal Revenue Code.

Annual 1099-DIV

2020 Common Stock Tax Information

NDP provides the following tax information to its common stockholders pertaining to the character of distributions paid during 2020. For stockholders who received all distributions in cash during 2020, approximately 0.00% was treated as ordinary income (Box 1a less Box 1b), 0.06% as qualified dividend income (Box 1b), and approximately 99.94% was treated as a return of capital (Box 3). The per share characterization is reflected in the sample Form 1099-DIV below.

| Ex-Div Date | Record Date | Payment Date | Total Distributions Per Share | Total Ordinary Dividends Box 1a 1 | Qualified Dividends Box 1b 2 | Capital Gain Distributions Box 2a 3 | Nondividend Distributions Box 3 4 | ||

|---|---|---|---|---|---|---|---|---|---|

| $2.775000 | $0.426800 | $0.426800 | $0.000000 | $2.348200 | |||||

| $2.520000 | $0.746900 | $0.746900 | $0.000000 | $1.773100 | |||||

| 12/31/2022 | 12/31/2022 | 12/31/2022 | $2.080000 | $0.821900 | $0.821900 | $0.000000 | $1.258100 | ||

| 1/01/2021 | 1/01/2021 | 1/01/2021 | $0.310000 | $0.023300 | $0.023300 | $0.000000 | $0.286700 | ||

| 2/20/2020 | 2/21/2020 | 2/28/2020 | $0.100000 | $0.000056 | $0.000056 | $0.000000 | $0.099944 | ||

| 11/20/2019 | 11/22/2019 | 11/29/2019 | $0.100000 | $0.000000 | $0.000000 | $0.000000 | $0.100000 | ||

| 8/21/2019 | 8/23/2019 | 8/30/2019 | $0.100000 | $0.000000 | $0.000000 | $0.000000 | $0.100000 | ||

| 5/22/2019 | 5/24/2019 | 5/31/2019 | $0.437500 | $0.000000 | $0.000000 | $0.000000 | $0.437500 | ||

| 2/21/2019 | 2/21/2019 | 2/28/2019 | $0.437500 | $0.000000 | $0.000000 | $0.000000 | $0.437500 | ||

| 11/22/2018 | 11/23/2018 | 11/30/2018 | $0.437500 | $0.000000 | $0.000000 | $0.000000 | $0.437500 | ||

| 8/23/2018 | 8/24/2018 | 8/31/2018 | $0.437500 | $0.000000 | $0.000000 | $0.000000 | $0.437500 | ||

| 5/23/2018 | 5/24/2018 | 5/31/2018 | $0.437500 | $0.000000 | $0.000000 | $0.000000 | $0.437500 | ||

| 2/20/2018 | 2/21/2018 | 2/28/2018 | $0.437500 | $0.000000 | $0.000000 | $0.000000 | $0.437500 | ||

| 11/21/2017 | 11/22/2017 | 11/30/2017 | $0.437500 | $0.000000 | $0.000000 | $0.000000 | $0.437500 | ||

| 8/22/2017 | 8/24/2017 | 8/31/2017 | $0.437500 | $0.000000 | $0.000000 | $0.000000 | $0.437500 | ||

| 5/22/2017 | 5/24/2017 | 5/31/2017 | $0.437500 | $0.000000 | $0.000000 | $0.000000 | $0.437500 | ||

| 2/16/2017 | 2/21/2017 | 2/28/2017 | $0.437500 | $0.000000 | $0.000000 | $0.000000 | $0.437500 | ||

| 8/22/2016 | 8/24/2016 | 8/31/2016 | $0.437500 | $0.000000 | $0.000000 | $0.000000 | $0.437500 | ||

| 5/20/2016 | 5/24/2016 | 5/31/2016 | $0.437500 | $0.000000 | $0.000000 | $0.000000 | $0.437500 | ||

| 2/18/2016 | 2/22/2016 | 2/29/2016 | $0.437500 | $0.000000 | $0.000000 | $0.000000 | $0.437500 | ||

| 1/21/2016 | 11/23/2016 | 11/30/2016 | $0.437500 | $0.000000 | $0.000000 | $0.000000 | $0.437500 | ||

| 11/19/2015 | 11/23/2015 | 11/30/2015 | $0.437500 | $0.000135 | $0.000135 | $0.000000 | $0.437365 | ||

| 8/20/2015 | 8/24/2015 | 8/31/2015 | $0.437500 | $0.000135 | $0.000135 | $0.000000 | $0.437365 | ||

| 5/20/2015 | 5/22/2015 | 5/29/2015 | $0.437500 | $0.000135 | $0.000135 | $0.000000 | $0.437365 | ||

| 2/18/2015 | 2/20/2015 | 2/27/2015 | $0.437500 | $0.000135 | $0.000135 | $0.000000 | $0.437365 | ||

| 11/19/2014 | 11/21/2014 | 11/28/2014 | $0.437500 | $0.296834 | $0.052126 | $0.118581 | $0.022085 | ||

| 8/20/2014 | 8/22/2014 | 8/29/2014 | $0.437500 | $0.296834 | $0.052126 | $0.118581 | $0.022085 | ||

| 5/20/2014 | 5/22/2014 | 5/30/2014 | $0.437500 | $0.296834 | $0.052126 | $0.118581 | $0.022085 | ||

| 2/19/2014 | 2/21/2014 | 2/28/2014 | $0.437500 | $0.296834 | $0.052126 | $0.118581 | $0.022085 | ||

| 11/20/2013 | 11/22/2013 | 11/29/2013 | $0.437500 | $0.407647 | $0.064480 | $0.015117 | $0.014736 | ||

| 8/21/2013 | 8/23/2013 | 9/03/2013 | $0.437500 | $0.407647 | $0.064480 | $0.015117 | $0.014736 | ||

| 5/21/2013 | 5/23/2013 | 6/03/2013 | $0.437500 | $0.407647 | $0.064480 | $0.015117 | $0.014736 | ||

| 2/19/2013 | 2/21/2013 | 3/01/2013 | $0.437500 | $0.407647 | $0.064480 | $0.015117 | $0.014736 | ||

| 11/20/2012 | 11/23/2012 | 11/30/2012 | $0.437500 | $0.389009 | $0.090256 | $0.000000 | $0.048491 | ||

| Total 2020 Distributions: | $19.797500 | $5.226429 | $2.576176 | $0.534792 | $14.036279 | ||||

-

Box 1a: Ordinary dividends are taxed at ordinary income tax rates.

-

Box 1b: Qualified dividends are taxed at capital gain tax rates if the stockholder meets holding period requirements.

-

Box 2a: Capital gain distributions (long-term) are taxed at capital gain tax rates.

-

Box 3: Nondividend distributions are nontaxable and considered return of capital.

For stockholders who participated in the company sponsored dividend reinvestment plan, the tax basis of shares acquired is the greater of the purchase price or the market close price on the payment date.

Report of Organizational Actions Affecting Basis of Securities

Effective January 1, 2012, issuers of regulated investment company securities must complete Form 8937 to report organizational actions, including nontaxable distributions, that affect the basis of the securities involved in the organizational action. The information contained below is intended to satisfy the requirements of public reporting under section 1.6045B-1(a)(3) and (b)(4) of the Treasury Regulations.

Nothing contained herein should be construed as tax advice; consult your tax adviser for more information. Furthermore, you may not rely upon any information herein for the purpose of avoiding any penalties that may be imposed under the Internal Revenue Code.

Annual 1099-DIV

2019 Common Stock Tax Information

NDP provides the following tax information to its common stockholders pertaining to the character of distributions paid during 2019. For stockholders who received all distributions in cash during 2019, 100% was treated as a return of capital (Box 3). The per share characterization is reflected in the sample Form 1099-DIV below.

| Ex-Div Date | Record Date | Payment Date | Total Distributions Per Share | Total Ordinary Dividends Box 1a 1 | Qualified Dividends Box 1b 2 | Capital Gain Distributions Box 2a 3 | Nondividend Distributions Box 3 4 | ||

|---|---|---|---|---|---|---|---|---|---|

| $2.775000 | $0.426800 | $0.426800 | $0.000000 | $2.348200 | |||||

| $2.520000 | $0.746900 | $0.746900 | $0.000000 | $1.773100 | |||||

| 12/31/2022 | 12/31/2022 | 12/31/2022 | $2.080000 | $0.821900 | $0.821900 | $0.000000 | $1.258100 | ||

| 1/01/2021 | 1/01/2021 | 1/01/2021 | $0.310000 | $0.023300 | $0.023300 | $0.000000 | $0.286700 | ||

| 2/20/2020 | 2/21/2020 | 2/28/2020 | $0.100000 | $0.000056 | $0.000056 | $0.000000 | $0.099944 | ||

| 11/20/2019 | 11/22/2019 | 11/29/2019 | $0.100000 | $0.000000 | $0.000000 | $0.000000 | $0.100000 | ||

| 8/21/2019 | 8/23/2019 | 8/30/2019 | $0.100000 | $0.000000 | $0.000000 | $0.000000 | $0.100000 | ||

| 5/22/2019 | 5/24/2019 | 5/31/2019 | $0.437500 | $0.000000 | $0.000000 | $0.000000 | $0.437500 | ||

| 2/21/2019 | 2/21/2019 | 2/28/2019 | $0.437500 | $0.000000 | $0.000000 | $0.000000 | $0.437500 | ||

| 11/22/2018 | 11/23/2018 | 11/30/2018 | $0.437500 | $0.000000 | $0.000000 | $0.000000 | $0.437500 | ||

| 8/23/2018 | 8/24/2018 | 8/31/2018 | $0.437500 | $0.000000 | $0.000000 | $0.000000 | $0.437500 | ||

| 5/23/2018 | 5/24/2018 | 5/31/2018 | $0.437500 | $0.000000 | $0.000000 | $0.000000 | $0.437500 | ||

| 2/20/2018 | 2/21/2018 | 2/28/2018 | $0.437500 | $0.000000 | $0.000000 | $0.000000 | $0.437500 | ||

| 11/21/2017 | 11/22/2017 | 11/30/2017 | $0.437500 | $0.000000 | $0.000000 | $0.000000 | $0.437500 | ||

| 8/22/2017 | 8/24/2017 | 8/31/2017 | $0.437500 | $0.000000 | $0.000000 | $0.000000 | $0.437500 | ||

| 5/22/2017 | 5/24/2017 | 5/31/2017 | $0.437500 | $0.000000 | $0.000000 | $0.000000 | $0.437500 | ||

| 2/16/2017 | 2/21/2017 | 2/28/2017 | $0.437500 | $0.000000 | $0.000000 | $0.000000 | $0.437500 | ||

| 8/22/2016 | 8/24/2016 | 8/31/2016 | $0.437500 | $0.000000 | $0.000000 | $0.000000 | $0.437500 | ||

| 5/20/2016 | 5/24/2016 | 5/31/2016 | $0.437500 | $0.000000 | $0.000000 | $0.000000 | $0.437500 | ||

| 2/18/2016 | 2/22/2016 | 2/29/2016 | $0.437500 | $0.000000 | $0.000000 | $0.000000 | $0.437500 | ||

| 1/21/2016 | 11/23/2016 | 11/30/2016 | $0.437500 | $0.000000 | $0.000000 | $0.000000 | $0.437500 | ||

| 11/19/2015 | 11/23/2015 | 11/30/2015 | $0.437500 | $0.000135 | $0.000135 | $0.000000 | $0.437365 | ||

| 8/20/2015 | 8/24/2015 | 8/31/2015 | $0.437500 | $0.000135 | $0.000135 | $0.000000 | $0.437365 | ||

| 5/20/2015 | 5/22/2015 | 5/29/2015 | $0.437500 | $0.000135 | $0.000135 | $0.000000 | $0.437365 | ||

| 2/18/2015 | 2/20/2015 | 2/27/2015 | $0.437500 | $0.000135 | $0.000135 | $0.000000 | $0.437365 | ||

| 11/19/2014 | 11/21/2014 | 11/28/2014 | $0.437500 | $0.296834 | $0.052126 | $0.118581 | $0.022085 | ||

| 8/20/2014 | 8/22/2014 | 8/29/2014 | $0.437500 | $0.296834 | $0.052126 | $0.118581 | $0.022085 | ||

| 5/20/2014 | 5/22/2014 | 5/30/2014 | $0.437500 | $0.296834 | $0.052126 | $0.118581 | $0.022085 | ||

| 2/19/2014 | 2/21/2014 | 2/28/2014 | $0.437500 | $0.296834 | $0.052126 | $0.118581 | $0.022085 | ||

| 11/20/2013 | 11/22/2013 | 11/29/2013 | $0.437500 | $0.407647 | $0.064480 | $0.015117 | $0.014736 | ||

| 8/21/2013 | 8/23/2013 | 9/03/2013 | $0.437500 | $0.407647 | $0.064480 | $0.015117 | $0.014736 | ||

| 5/21/2013 | 5/23/2013 | 6/03/2013 | $0.437500 | $0.407647 | $0.064480 | $0.015117 | $0.014736 | ||

| 2/19/2013 | 2/21/2013 | 3/01/2013 | $0.437500 | $0.407647 | $0.064480 | $0.015117 | $0.014736 | ||

| 11/20/2012 | 11/23/2012 | 11/30/2012 | $0.437500 | $0.389009 | $0.090256 | $0.000000 | $0.048491 | ||

| Total 2019 Distributions: | $19.797500 | $5.226429 | $2.576176 | $0.534792 | $14.036279 | ||||

-

Box 1a: Ordinary dividends are taxed at ordinary income tax rates.

-

Box 1b: Qualified dividends are taxed at capital gain tax rates if the stockholder meets holding period requirements.

-

Box 2a: Capital gain distributions (long-term) are taxed at capital gain tax rates.

-

Box 3: Nondividend distributions are nontaxable and considered return of capital.

For stockholders who participated in the company sponsored dividend reinvestment plan, the tax basis of shares acquired is the greater of the purchase price or the market close price on the payment date.

Report of Organizational Actions Affecting Basis of Securities

Effective January 1, 2012, issuers of regulated investment company securities must complete Form 8937 to report organizational actions, including nontaxable distributions, that affect the basis of the securities involved in the organizational action. The information contained below is intended to satisfy the requirements of public reporting under section 1.6045B-1(a)(3) and (b)(4) of the Treasury Regulations.

Nothing contained herein should be construed as tax advice; consult your tax advisor for more information. Furthermore, you may not rely upon any information herein for the purpose of avoiding any penalties that may be imposed under the Internal Revenue Code.

Annual 1099-DIV

2018 Common Stock Tax Information

NDP provides the following tax information to its common stockholders pertaining to the character of distributions paid during 2018. For stockholders who received all distributions in cash during 2018, 100% was treated as a return of capital (Box 3). The per share characterization is reflected in the sample Form 1099-DIV below.

| Ex-Div Date | Record Date | Payment Date | Total Distributions Per Share | Total Ordinary Dividends Box 1a 1 | Qualified Dividends Box 1b 2 | Capital Gain Distributions Box 2a | Nondividend Distributions Box 3 3 | ||

|---|---|---|---|---|---|---|---|---|---|

| $2.775000 | $0.426800 | $0.426800 | $0.000000 | $2.348200 | |||||

| $2.520000 | $0.746900 | $0.746900 | $0.000000 | $1.773100 | |||||

| 12/31/2022 | 12/31/2022 | 12/31/2022 | $2.080000 | $0.821900 | $0.821900 | $0.000000 | $1.258100 | ||

| 1/01/2021 | 1/01/2021 | 1/01/2021 | $0.310000 | $0.023300 | $0.023300 | $0.000000 | $0.286700 | ||

| 2/20/2020 | 2/21/2020 | 2/28/2020 | $0.100000 | $0.000056 | $0.000056 | $0.000000 | $0.099944 | ||

| 11/20/2019 | 11/22/2019 | 11/29/2019 | $0.100000 | $0.000000 | $0.000000 | $0.000000 | $0.100000 | ||

| 8/21/2019 | 8/23/2019 | 8/30/2019 | $0.100000 | $0.000000 | $0.000000 | $0.000000 | $0.100000 | ||

| 5/22/2019 | 5/24/2019 | 5/31/2019 | $0.437500 | $0.000000 | $0.000000 | $0.000000 | $0.437500 | ||

| 2/21/2019 | 2/21/2019 | 2/28/2019 | $0.437500 | $0.000000 | $0.000000 | $0.000000 | $0.437500 | ||

| 11/22/2018 | 11/23/2018 | 11/30/2018 | $0.437500 | $0.000000 | $0.000000 | $0.000000 | $0.437500 | ||

| 8/23/2018 | 8/24/2018 | 8/31/2018 | $0.437500 | $0.000000 | $0.000000 | $0.000000 | $0.437500 | ||

| 5/23/2018 | 5/24/2018 | 5/31/2018 | $0.437500 | $0.000000 | $0.000000 | $0.000000 | $0.437500 | ||

| 2/20/2018 | 2/21/2018 | 2/28/2018 | $0.437500 | $0.000000 | $0.000000 | $0.000000 | $0.437500 | ||

| 11/21/2017 | 11/22/2017 | 11/30/2017 | $0.437500 | $0.000000 | $0.000000 | $0.000000 | $0.437500 | ||

| 8/22/2017 | 8/24/2017 | 8/31/2017 | $0.437500 | $0.000000 | $0.000000 | $0.000000 | $0.437500 | ||

| 5/22/2017 | 5/24/2017 | 5/31/2017 | $0.437500 | $0.000000 | $0.000000 | $0.000000 | $0.437500 | ||

| 2/16/2017 | 2/21/2017 | 2/28/2017 | $0.437500 | $0.000000 | $0.000000 | $0.000000 | $0.437500 | ||

| 8/22/2016 | 8/24/2016 | 8/31/2016 | $0.437500 | $0.000000 | $0.000000 | $0.000000 | $0.437500 | ||

| 5/20/2016 | 5/24/2016 | 5/31/2016 | $0.437500 | $0.000000 | $0.000000 | $0.000000 | $0.437500 | ||

| 2/18/2016 | 2/22/2016 | 2/29/2016 | $0.437500 | $0.000000 | $0.000000 | $0.000000 | $0.437500 | ||

| 1/21/2016 | 11/23/2016 | 11/30/2016 | $0.437500 | $0.000000 | $0.000000 | $0.000000 | $0.437500 | ||

| 11/19/2015 | 11/23/2015 | 11/30/2015 | $0.437500 | $0.000135 | $0.000135 | $0.000000 | $0.437365 | ||

| 8/20/2015 | 8/24/2015 | 8/31/2015 | $0.437500 | $0.000135 | $0.000135 | $0.000000 | $0.437365 | ||

| 5/20/2015 | 5/22/2015 | 5/29/2015 | $0.437500 | $0.000135 | $0.000135 | $0.000000 | $0.437365 | ||

| 2/18/2015 | 2/20/2015 | 2/27/2015 | $0.437500 | $0.000135 | $0.000135 | $0.000000 | $0.437365 | ||

| 11/19/2014 | 11/21/2014 | 11/28/2014 | $0.437500 | $0.296834 | $0.052126 | $0.118581 | $0.022085 | ||

| 8/20/2014 | 8/22/2014 | 8/29/2014 | $0.437500 | $0.296834 | $0.052126 | $0.118581 | $0.022085 | ||

| 5/20/2014 | 5/22/2014 | 5/30/2014 | $0.437500 | $0.296834 | $0.052126 | $0.118581 | $0.022085 | ||

| 2/19/2014 | 2/21/2014 | 2/28/2014 | $0.437500 | $0.296834 | $0.052126 | $0.118581 | $0.022085 | ||

| 11/20/2013 | 11/22/2013 | 11/29/2013 | $0.437500 | $0.407647 | $0.064480 | $0.015117 | $0.014736 | ||

| 8/21/2013 | 8/23/2013 | 9/03/2013 | $0.437500 | $0.407647 | $0.064480 | $0.015117 | $0.014736 | ||

| 5/21/2013 | 5/23/2013 | 6/03/2013 | $0.437500 | $0.407647 | $0.064480 | $0.015117 | $0.014736 | ||

| 2/19/2013 | 2/21/2013 | 3/01/2013 | $0.437500 | $0.407647 | $0.064480 | $0.015117 | $0.014736 | ||

| 11/20/2012 | 11/23/2012 | 11/30/2012 | $0.437500 | $0.389009 | $0.090256 | $0.000000 | $0.048491 | ||

| Total 2018 Distributions: | $19.797500 | $5.226429 | $2.576176 | $0.534792 | $14.036279 | ||||

-

Box 1a: Ordinary dividends are taxed at ordinary income tax rates.

-

Box 1b: Qualified dividends are taxed at capital gain tax rates if the stockholder meets holding period requirements.

-

Box 3: Nondividend distributions are nontaxable and considered return of capital.

For stockholders who participated in the company sponsored dividend reinvestment plan, the tax basis of shares acquired is the greater of the purchase price or the market close price on the payment date.

Report of Organizational Actions Affecting Basis of Securities

Effective January 1, 2012, issuers of regulated investment company securities must complete Form 8937 to report organizational actions, including nontaxable distributions, that affect the basis of the securities involved in the organizational action. The information contained below is intended to satisfy the requirements of public reporting under section 1.6045B-1(a)(3) and (b)(4) of the Treasury Regulations.

Nothing contained herein should be construed as tax advice; consult your tax advisor for more information. Furthermore, you may not rely upon any information herein for the purpose of avoiding any penalties that may be imposed under the Internal Revenue Code.

Annual 1099-DIV

2017 Common Stock Tax Information

NDP provides the following tax information to its common stockholders pertaining to the character of distributions paid during 2017. For stockholders who received all distributions in cash during 2017, 100% was treated as a return of capital (Box 3). The per share characterization is reflected in the sample Form 1099-DIV below.

| Ex-Div Date | Record Date | Payment Date | Total Distributions Per Share | Total Ordinary Dividends Box 1a | Qualified Dividends Box 1b | Capital Gain Distributions Box 2a | Nondividend Distributions Box 3 1 | ||

|---|---|---|---|---|---|---|---|---|---|

| $2.78 | $0.43 | $0.43 | $0.00 | $2.35 | |||||

| $2.52 | $0.75 | $0.75 | $0.00 | $1.77 | |||||

| 12/31/2022 | 12/31/2022 | 12/31/2022 | $2.08 | $0.82 | $0.82 | $0.00 | $1.26 | ||

| 1/01/2021 | 1/01/2021 | 1/01/2021 | $0.31 | $0.02 | $0.02 | $0.00 | $0.29 | ||

| 2/20/2020 | 2/21/2020 | 2/28/2020 | $0.10 | $0.00 | $0.00 | $0.00 | $0.10 | ||

| 11/20/2019 | 11/22/2019 | 11/29/2019 | $0.10 | $0.00 | $0.00 | $0.00 | $0.10 | ||

| 8/21/2019 | 8/23/2019 | 8/30/2019 | $0.10 | $0.00 | $0.00 | $0.00 | $0.10 | ||

| 5/22/2019 | 5/24/2019 | 5/31/2019 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 2/21/2019 | 2/21/2019 | 2/28/2019 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 11/22/2018 | 11/23/2018 | 11/30/2018 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 8/23/2018 | 8/24/2018 | 8/31/2018 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 5/23/2018 | 5/24/2018 | 5/31/2018 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 2/20/2018 | 2/21/2018 | 2/28/2018 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 11/21/2017 | 11/22/2017 | 11/30/2017 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 8/22/2017 | 8/24/2017 | 8/31/2017 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 5/22/2017 | 5/24/2017 | 5/31/2017 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 2/16/2017 | 2/21/2017 | 2/28/2017 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 8/22/2016 | 8/24/2016 | 8/31/2016 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 5/20/2016 | 5/24/2016 | 5/31/2016 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 2/18/2016 | 2/22/2016 | 2/29/2016 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 1/21/2016 | 11/23/2016 | 11/30/2016 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 11/19/2015 | 11/23/2015 | 11/30/2015 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 8/20/2015 | 8/24/2015 | 8/31/2015 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 5/20/2015 | 5/22/2015 | 5/29/2015 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 2/18/2015 | 2/20/2015 | 2/27/2015 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 11/19/2014 | 11/21/2014 | 11/28/2014 | $0.44 | $0.30 | $0.05 | $0.12 | $0.02 | ||

| 8/20/2014 | 8/22/2014 | 8/29/2014 | $0.44 | $0.30 | $0.05 | $0.12 | $0.02 | ||

| 5/20/2014 | 5/22/2014 | 5/30/2014 | $0.44 | $0.30 | $0.05 | $0.12 | $0.02 | ||

| 2/19/2014 | 2/21/2014 | 2/28/2014 | $0.44 | $0.30 | $0.05 | $0.12 | $0.02 | ||

| 11/20/2013 | 11/22/2013 | 11/29/2013 | $0.44 | $0.41 | $0.06 | $0.02 | $0.01 | ||

| 8/21/2013 | 8/23/2013 | 9/03/2013 | $0.44 | $0.41 | $0.06 | $0.02 | $0.01 | ||

| 5/21/2013 | 5/23/2013 | 6/03/2013 | $0.44 | $0.41 | $0.06 | $0.02 | $0.01 | ||

| 2/19/2013 | 2/21/2013 | 3/01/2013 | $0.44 | $0.41 | $0.06 | $0.02 | $0.01 | ||

| 11/20/2012 | 11/23/2012 | 11/30/2012 | $0.44 | $0.39 | $0.09 | $0.00 | $0.05 | ||

| Total 2017 Distributions: | $19.80 | $5.23 | $2.58 | $0.53 | $14.04 | ||||

-

Box 3: Nondividend distributions are nontaxable and considered return of capital.

For stockholders who participated in the company sponsored dividend reinvestment plan, the tax basis of shares acquired is the greater of the purchase price or the market close price on the payment date.

Report of Organizational Actions Affecting Basis of Securities

Effective January 1, 2012, issuers of regulated investment company securities must complete Form 8937 to report organizational actions, including nontaxable distributions, that affect the basis of the securities involved in the organizational action. The information contained below is intended to satisfy the requirements of public reporting under section 1.6045B-1(a)(3) and (b)(4) of the Treasury Regulations.

Nothing contained herein should be construed as tax advice; consult your tax advisor for more information. Furthermore, you may not rely upon any information herein for the purpose of avoiding any penalties that may be imposed under the Internal Revenue Code.

Annual 1099-DIV

2016 Common Stock Tax Information

NDP provides the following tax information to its common stockholders pertaining to the character of distributions paid during 2016. For stockholders who received all distributions in cash during 2016, 100% was treated as a return of capital (Box 3). The per share characterization is reflected in the sample Form 1099-DIV below.

| Ex-Div Date | Record Date | Payment Date | Total Distributions Per Share | Total Ordinary Dividends Box 1a | Qualified Dividends Box 1b | Capital Gain Distributions Box 2a | Nondividend Distributions Box 3 1 | ||

|---|---|---|---|---|---|---|---|---|---|

| $2.78 | $0.43 | $0.43 | $0.00 | $2.35 | |||||

| $2.52 | $0.75 | $0.75 | $0.00 | $1.77 | |||||

| 12/31/2022 | 12/31/2022 | 12/31/2022 | $2.08 | $0.82 | $0.82 | $0.00 | $1.26 | ||

| 1/01/2021 | 1/01/2021 | 1/01/2021 | $0.31 | $0.02 | $0.02 | $0.00 | $0.29 | ||

| 2/20/2020 | 2/21/2020 | 2/28/2020 | $0.10 | $0.00 | $0.00 | $0.00 | $0.10 | ||

| 11/20/2019 | 11/22/2019 | 11/29/2019 | $0.10 | $0.00 | $0.00 | $0.00 | $0.10 | ||

| 8/21/2019 | 8/23/2019 | 8/30/2019 | $0.10 | $0.00 | $0.00 | $0.00 | $0.10 | ||

| 5/22/2019 | 5/24/2019 | 5/31/2019 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 2/21/2019 | 2/21/2019 | 2/28/2019 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 11/22/2018 | 11/23/2018 | 11/30/2018 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 8/23/2018 | 8/24/2018 | 8/31/2018 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 5/23/2018 | 5/24/2018 | 5/31/2018 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 2/20/2018 | 2/21/2018 | 2/28/2018 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 11/21/2017 | 11/22/2017 | 11/30/2017 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 8/22/2017 | 8/24/2017 | 8/31/2017 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 5/22/2017 | 5/24/2017 | 5/31/2017 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 2/16/2017 | 2/21/2017 | 2/28/2017 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 8/22/2016 | 8/24/2016 | 8/31/2016 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 5/20/2016 | 5/24/2016 | 5/31/2016 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 2/18/2016 | 2/22/2016 | 2/29/2016 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 1/21/2016 | 11/23/2016 | 11/30/2016 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 11/19/2015 | 11/23/2015 | 11/30/2015 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 8/20/2015 | 8/24/2015 | 8/31/2015 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 5/20/2015 | 5/22/2015 | 5/29/2015 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 2/18/2015 | 2/20/2015 | 2/27/2015 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 11/19/2014 | 11/21/2014 | 11/28/2014 | $0.44 | $0.30 | $0.05 | $0.12 | $0.02 | ||

| 8/20/2014 | 8/22/2014 | 8/29/2014 | $0.44 | $0.30 | $0.05 | $0.12 | $0.02 | ||

| 5/20/2014 | 5/22/2014 | 5/30/2014 | $0.44 | $0.30 | $0.05 | $0.12 | $0.02 | ||

| 2/19/2014 | 2/21/2014 | 2/28/2014 | $0.44 | $0.30 | $0.05 | $0.12 | $0.02 | ||

| 11/20/2013 | 11/22/2013 | 11/29/2013 | $0.44 | $0.41 | $0.06 | $0.02 | $0.01 | ||

| 8/21/2013 | 8/23/2013 | 9/03/2013 | $0.44 | $0.41 | $0.06 | $0.02 | $0.01 | ||

| 5/21/2013 | 5/23/2013 | 6/03/2013 | $0.44 | $0.41 | $0.06 | $0.02 | $0.01 | ||

| 2/19/2013 | 2/21/2013 | 3/01/2013 | $0.44 | $0.41 | $0.06 | $0.02 | $0.01 | ||

| 11/20/2012 | 11/23/2012 | 11/30/2012 | $0.44 | $0.39 | $0.09 | $0.00 | $0.05 | ||

| Total 2016 Distributions: | $19.80 | $5.23 | $2.58 | $0.53 | $14.04 | ||||

-

Box 3: Nondividend distributions are nontaxable and considered return of capital.

For stockholders who participated in the company sponsored dividend reinvestment plan, the tax basis of shares acquired is the greater of the purchase price or the market close price on the payment date.

Report of Organizational Actions Affecting Basis of Securities

Effective January 1, 2012, issuers of regulated investment company securities must complete Form 8937 to report organizational actions, including nontaxable distributions, that affect the basis of the securities involved in the organizational action. The information contained below is intended to satisy the requirements of public reporting under section 1.6045B-1(a)(3) and (b)(4) of the Treasury Regulations.

Nothing contained herein should be construed as tax advice; consult your tax advisor for more information. Furthermore, you may not rely upon any information herein for the purpose of avoiding any penalties that may be imposed under the Internal Revenue Code.

Annual 1099-DIV

2015 Common Stock Tax Information

NDP provides the following tax information to its common stockholders pertaining to the character of distributions paid during 2015. For stockholders who received all distributions in cash during 2015, 0.03% was treated as qualified dividend income (Box 1b) and 99.97% as a return of capital (Box 3). The per share characterization is reflected in the sample Form 1099-DIV below.

| Ex-Div Date | Record Date | Payment Date | Total Distributions Per Share | Total Ordinary Dividends Box 1a 1 | Qualified Dividends Box 1b 2 | Capital Gain Distributions Box 2a | Nondividend Distributions Box 3 3 | ||

|---|---|---|---|---|---|---|---|---|---|

| $2.78 | $0.43 | $0.43 | $0.00 | $2.35 | |||||

| $2.52 | $0.75 | $0.75 | $0.00 | $1.77 | |||||

| 12/31/2022 | 12/31/2022 | 12/31/2022 | $2.08 | $0.82 | $0.82 | $0.00 | $1.26 | ||

| 1/01/2021 | 1/01/2021 | 1/01/2021 | $0.31 | $0.02 | $0.02 | $0.00 | $0.29 | ||

| 2/20/2020 | 2/21/2020 | 2/28/2020 | $0.10 | $0.00 | $0.00 | $0.00 | $0.10 | ||

| 11/20/2019 | 11/22/2019 | 11/29/2019 | $0.10 | $0.00 | $0.00 | $0.00 | $0.10 | ||

| 8/21/2019 | 8/23/2019 | 8/30/2019 | $0.10 | $0.00 | $0.00 | $0.00 | $0.10 | ||

| 5/22/2019 | 5/24/2019 | 5/31/2019 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 2/21/2019 | 2/21/2019 | 2/28/2019 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 11/22/2018 | 11/23/2018 | 11/30/2018 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 8/23/2018 | 8/24/2018 | 8/31/2018 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 5/23/2018 | 5/24/2018 | 5/31/2018 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 2/20/2018 | 2/21/2018 | 2/28/2018 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 11/21/2017 | 11/22/2017 | 11/30/2017 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 8/22/2017 | 8/24/2017 | 8/31/2017 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 5/22/2017 | 5/24/2017 | 5/31/2017 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 2/16/2017 | 2/21/2017 | 2/28/2017 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 8/22/2016 | 8/24/2016 | 8/31/2016 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 5/20/2016 | 5/24/2016 | 5/31/2016 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 2/18/2016 | 2/22/2016 | 2/29/2016 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 1/21/2016 | 11/23/2016 | 11/30/2016 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 11/19/2015 | 11/23/2015 | 11/30/2015 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 8/20/2015 | 8/24/2015 | 8/31/2015 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 5/20/2015 | 5/22/2015 | 5/29/2015 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 2/18/2015 | 2/20/2015 | 2/27/2015 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 11/19/2014 | 11/21/2014 | 11/28/2014 | $0.44 | $0.30 | $0.05 | $0.12 | $0.02 | ||

| 8/20/2014 | 8/22/2014 | 8/29/2014 | $0.44 | $0.30 | $0.05 | $0.12 | $0.02 | ||

| 5/20/2014 | 5/22/2014 | 5/30/2014 | $0.44 | $0.30 | $0.05 | $0.12 | $0.02 | ||

| 2/19/2014 | 2/21/2014 | 2/28/2014 | $0.44 | $0.30 | $0.05 | $0.12 | $0.02 | ||

| 11/20/2013 | 11/22/2013 | 11/29/2013 | $0.44 | $0.41 | $0.06 | $0.02 | $0.01 | ||

| 8/21/2013 | 8/23/2013 | 9/03/2013 | $0.44 | $0.41 | $0.06 | $0.02 | $0.01 | ||

| 5/21/2013 | 5/23/2013 | 6/03/2013 | $0.44 | $0.41 | $0.06 | $0.02 | $0.01 | ||

| 2/19/2013 | 2/21/2013 | 3/01/2013 | $0.44 | $0.41 | $0.06 | $0.02 | $0.01 | ||

| 11/20/2012 | 11/23/2012 | 11/30/2012 | $0.44 | $0.39 | $0.09 | $0.00 | $0.05 | ||

| Total 2015 Distributions: | $19.80 | $5.23 | $2.58 | $0.53 | $14.04 | ||||

-

Box 1a: Ordinary dividends are taxed at ordinary income tax rates.

-

Box 1b: Qualified dividends are taxed at capital gain tax rates if the stockholder meets holding period requirements.

-

Box 3: Nondividend distributions are nontaxable and considered return of capital.

For stockholders who participated in the company sponsored dividend reinvestment plan, the tax basis of shares acquired is the greater of the purchase price or the market close price on the payment date.

Report of Organizational Actions Affecting Basis of Securities

Effective January 1, 2012, issuers of regulated investment company securities must complete Form 8937 to report organizational actions, including nontaxable distributions, that affect the basis of the securities involved in the organizational action. The information contained below is intended to satisy the requirements of public reporting under section 1.6045B-1(a)(3) and (b)(4) of the Treasury Regulations.

Nothing contained herein should be construed as tax advice; consult your tax advisor for more information. Furthermore, you may not rely upon any information herein for the purpose of avoiding any penalties that may be imposed under the Internal Revenue Code.

Annual 1099-DIV

2014 Common Stock Tax Information

NDP provides the following tax information to its common stockholders pertaining to the character of distributions paid during 2014. For stockholders who received all distributions in cash during 2014, 55.93% was treated as ordinary income (Box 1a less Box 1b), 11.92% as qualified dividend income (Box 1b), 27.10% as capital gain (Box 2a), and 5.05% as a return of capital (Box 3). The per share characterization is reflected in the sample Form 1099-DIV below.

| Ex-Div Date | Record Date | Payment Date | Total Distributions Per Share | Total Ordinary Dividends Box 1a 1 | Qualified Dividends Box 1b 2 | Capital Gain Distributions Box 2a 3 | Nondividend Distributions Box 3 4 | ||

|---|---|---|---|---|---|---|---|---|---|

| $2.78 | $0.43 | $0.43 | $0.00 | $2.35 | |||||

| $2.52 | $0.75 | $0.75 | $0.00 | $1.77 | |||||

| 12/31/2022 | 12/31/2022 | 12/31/2022 | $2.08 | $0.82 | $0.82 | $0.00 | $1.26 | ||

| 1/01/2021 | 1/01/2021 | 1/01/2021 | $0.31 | $0.02 | $0.02 | $0.00 | $0.29 | ||

| 2/20/2020 | 2/21/2020 | 2/28/2020 | $0.10 | $0.00 | $0.00 | $0.00 | $0.10 | ||

| 11/20/2019 | 11/22/2019 | 11/29/2019 | $0.10 | $0.00 | $0.00 | $0.00 | $0.10 | ||

| 8/21/2019 | 8/23/2019 | 8/30/2019 | $0.10 | $0.00 | $0.00 | $0.00 | $0.10 | ||

| 5/22/2019 | 5/24/2019 | 5/31/2019 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 2/21/2019 | 2/21/2019 | 2/28/2019 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 11/22/2018 | 11/23/2018 | 11/30/2018 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 8/23/2018 | 8/24/2018 | 8/31/2018 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 5/23/2018 | 5/24/2018 | 5/31/2018 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 2/20/2018 | 2/21/2018 | 2/28/2018 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 11/21/2017 | 11/22/2017 | 11/30/2017 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 8/22/2017 | 8/24/2017 | 8/31/2017 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 5/22/2017 | 5/24/2017 | 5/31/2017 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 2/16/2017 | 2/21/2017 | 2/28/2017 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 8/22/2016 | 8/24/2016 | 8/31/2016 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 5/20/2016 | 5/24/2016 | 5/31/2016 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 2/18/2016 | 2/22/2016 | 2/29/2016 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 1/21/2016 | 11/23/2016 | 11/30/2016 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 11/19/2015 | 11/23/2015 | 11/30/2015 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 8/20/2015 | 8/24/2015 | 8/31/2015 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 5/20/2015 | 5/22/2015 | 5/29/2015 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 2/18/2015 | 2/20/2015 | 2/27/2015 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 11/19/2014 | 11/21/2014 | 11/28/2014 | $0.44 | $0.30 | $0.05 | $0.12 | $0.02 | ||

| 8/20/2014 | 8/22/2014 | 8/29/2014 | $0.44 | $0.30 | $0.05 | $0.12 | $0.02 | ||

| 5/20/2014 | 5/22/2014 | 5/30/2014 | $0.44 | $0.30 | $0.05 | $0.12 | $0.02 | ||

| 2/19/2014 | 2/21/2014 | 2/28/2014 | $0.44 | $0.30 | $0.05 | $0.12 | $0.02 | ||

| 11/20/2013 | 11/22/2013 | 11/29/2013 | $0.44 | $0.41 | $0.06 | $0.02 | $0.01 | ||

| 8/21/2013 | 8/23/2013 | 9/03/2013 | $0.44 | $0.41 | $0.06 | $0.02 | $0.01 | ||

| 5/21/2013 | 5/23/2013 | 6/03/2013 | $0.44 | $0.41 | $0.06 | $0.02 | $0.01 | ||

| 2/19/2013 | 2/21/2013 | 3/01/2013 | $0.44 | $0.41 | $0.06 | $0.02 | $0.01 | ||

| 11/20/2012 | 11/23/2012 | 11/30/2012 | $0.44 | $0.39 | $0.09 | $0.00 | $0.05 | ||

| Total 2014 Distributions: | $19.80 | $5.23 | $2.58 | $0.53 | $14.04 | ||||

-

Box 1a: Ordinary dividends are taxed at ordinary income tax rates.

-

Box 1b: Qualified dividends are taxed at capital gain tax rates if the stockholder meets holding period requirements.

-

Box 2a: Capital gain distributions (long-term) are taxed at capital gain tax rates.

-

Box 3: Nondividend distributions are nontaxable and considered return of capital.

For stockholders who participated in the company sponsored dividend reinvestment plan, the tax basis of shares acquired is the greater of the purchase price or the market close price on the payment date.

Report of Organizational Actions Affecting Basis of Securities

Effective January 1, 2012, issuers of regulated investment company securities must complete Form 8937 to report organizational actions, including nontaxable distributions, that affect the basis of the securities involved in the organizational action. The information contained below is intended to satisy the requirements of public reporting under section 1.6045B-1(a)(3) and (b)(4) of the Treasury Regulations.

Nothing contained herein should be construed as tax advice; consult your tax advisor for more information. Furthermore, you may not rely upon any information herein for the purpose of avoiding any penalties that may be imposed under the Internal Revenue Code.

Annual 1099-DIV

2013 Common Stock Tax Information

NDP provides the following tax information to its common stockholders pertaining to the character of distributions paid during 2013. For stockholders who received all distributions in cash during 2013, 78.44% was treated as ordinary income (Box 1a less Box 1b), 14.74% as qualified dividend income (Box 1b), 3.45% as capital gain (Box 2a), and 3.37% as a return of capital (Box 3). The per share characterization by quarter is reflected in the sample Form 1099-DIV below.

| Ex-Div Date | Record Date | Payment Date | Total Distributions Per Share | Total Ordinary Dividends Box 1a 1 | Qualified Dividends Box 1b 2 | Capital Gain Distributions Box 2a 3 | Nondividend Distributions Box 3 4 | ||

|---|---|---|---|---|---|---|---|---|---|

| $2.78 | $0.43 | $0.43 | $0.00 | $2.35 | |||||

| $2.52 | $0.75 | $0.75 | $0.00 | $1.77 | |||||

| 12/31/2022 | 12/31/2022 | 12/31/2022 | $2.08 | $0.82 | $0.82 | $0.00 | $1.26 | ||

| 1/01/2021 | 1/01/2021 | 1/01/2021 | $0.31 | $0.02 | $0.02 | $0.00 | $0.29 | ||

| 2/20/2020 | 2/21/2020 | 2/28/2020 | $0.10 | $0.00 | $0.00 | $0.00 | $0.10 | ||

| 11/20/2019 | 11/22/2019 | 11/29/2019 | $0.10 | $0.00 | $0.00 | $0.00 | $0.10 | ||

| 8/21/2019 | 8/23/2019 | 8/30/2019 | $0.10 | $0.00 | $0.00 | $0.00 | $0.10 | ||

| 5/22/2019 | 5/24/2019 | 5/31/2019 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 2/21/2019 | 2/21/2019 | 2/28/2019 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 11/22/2018 | 11/23/2018 | 11/30/2018 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 8/23/2018 | 8/24/2018 | 8/31/2018 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 5/23/2018 | 5/24/2018 | 5/31/2018 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 2/20/2018 | 2/21/2018 | 2/28/2018 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 11/21/2017 | 11/22/2017 | 11/30/2017 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 8/22/2017 | 8/24/2017 | 8/31/2017 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 5/22/2017 | 5/24/2017 | 5/31/2017 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 2/16/2017 | 2/21/2017 | 2/28/2017 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 8/22/2016 | 8/24/2016 | 8/31/2016 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 5/20/2016 | 5/24/2016 | 5/31/2016 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 2/18/2016 | 2/22/2016 | 2/29/2016 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 1/21/2016 | 11/23/2016 | 11/30/2016 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 11/19/2015 | 11/23/2015 | 11/30/2015 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 8/20/2015 | 8/24/2015 | 8/31/2015 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 5/20/2015 | 5/22/2015 | 5/29/2015 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 2/18/2015 | 2/20/2015 | 2/27/2015 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 11/19/2014 | 11/21/2014 | 11/28/2014 | $0.44 | $0.30 | $0.05 | $0.12 | $0.02 | ||

| 8/20/2014 | 8/22/2014 | 8/29/2014 | $0.44 | $0.30 | $0.05 | $0.12 | $0.02 | ||

| 5/20/2014 | 5/22/2014 | 5/30/2014 | $0.44 | $0.30 | $0.05 | $0.12 | $0.02 | ||

| 2/19/2014 | 2/21/2014 | 2/28/2014 | $0.44 | $0.30 | $0.05 | $0.12 | $0.02 | ||

| 11/20/2013 | 11/22/2013 | 11/29/2013 | $0.44 | $0.41 | $0.06 | $0.02 | $0.01 | ||

| 8/21/2013 | 8/23/2013 | 9/03/2013 | $0.44 | $0.41 | $0.06 | $0.02 | $0.01 | ||

| 5/21/2013 | 5/23/2013 | 6/03/2013 | $0.44 | $0.41 | $0.06 | $0.02 | $0.01 | ||

| 2/19/2013 | 2/21/2013 | 3/01/2013 | $0.44 | $0.41 | $0.06 | $0.02 | $0.01 | ||

| 11/20/2012 | 11/23/2012 | 11/30/2012 | $0.44 | $0.39 | $0.09 | $0.00 | $0.05 | ||

| Total 2013 Distributions: | $19.80 | $5.23 | $2.58 | $0.53 | $14.04 | ||||

-

Box 1a: Ordinary dividends are taxed at ordinary income tax rates.

-

Box 1b: Qualified dividends are taxed at capital gain tax rates if the stockholder meets holding period requirements.

-

Box 2a: Capital gain distributions (long-term) are taxed at capital gain tax rates.

-

Box 3: Nondividend distributions are nontaxable and considered return of capital.

For stockholders who participated in the company sponsored dividend reinvestment plan, the tax basis of shares acquired is the greater of the purchase price or the market close price on the payment date.

Report of Organizational Actions Affecting Basis of Securities

Effective January 1, 2012, issuers of regulated investment company securities must complete Form 8937 to report organizational actions, including nontaxable distributions, that affect the basis of the securities involved in the organizational action. The information contained below is intended to satisfy the requirements of public reporting under section 1.6045B-1(a)(3) and (b)(4) of the Treasury Regulations.

Nothing contained herein should be construed as tax advice; consult your tax advisor for more information. Furthermore, you may not rely upon any information herein for the purpose of avoiding any penalties that may be imposed under the Internal Revenue Code.

Annual 1099-DIV

2012 Common Stock Tax Information

NDP provides the following tax information to its common stockholders pertaining to the character of distributions paid during 2012. For stockholders who received all distributions in cash during 2012, approximately 68.29% was treated as ordinary income (Box 1a less Box 1b), 20.63% as qualified dividend income (Box 1b), and 11.08% as a return of capital (Box 3). The per share characterization by quarter is reflected in the sample Form 1099-DIV below.

| Ex-Div Date | Record Date | Payment Date | Total Distributions Per Share | Total Ordinary Dividends Box 1a 1 | Qualified Dividends Box 1b 2 | Capital Gain Distributions Box 2a | Nondividend Distributions Box 3 3 | ||

|---|---|---|---|---|---|---|---|---|---|

| $2.78 | $0.43 | $0.43 | $0.00 | $2.35 | |||||

| $2.52 | $0.75 | $0.75 | $0.00 | $1.77 | |||||

| 12/31/2022 | 12/31/2022 | 12/31/2022 | $2.08 | $0.82 | $0.82 | $0.00 | $1.26 | ||

| 1/01/2021 | 1/01/2021 | 1/01/2021 | $0.31 | $0.02 | $0.02 | $0.00 | $0.29 | ||

| 2/20/2020 | 2/21/2020 | 2/28/2020 | $0.10 | $0.00 | $0.00 | $0.00 | $0.10 | ||

| 11/20/2019 | 11/22/2019 | 11/29/2019 | $0.10 | $0.00 | $0.00 | $0.00 | $0.10 | ||

| 8/21/2019 | 8/23/2019 | 8/30/2019 | $0.10 | $0.00 | $0.00 | $0.00 | $0.10 | ||

| 5/22/2019 | 5/24/2019 | 5/31/2019 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 2/21/2019 | 2/21/2019 | 2/28/2019 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 11/22/2018 | 11/23/2018 | 11/30/2018 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 8/23/2018 | 8/24/2018 | 8/31/2018 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 5/23/2018 | 5/24/2018 | 5/31/2018 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 2/20/2018 | 2/21/2018 | 2/28/2018 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 11/21/2017 | 11/22/2017 | 11/30/2017 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 8/22/2017 | 8/24/2017 | 8/31/2017 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 5/22/2017 | 5/24/2017 | 5/31/2017 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 2/16/2017 | 2/21/2017 | 2/28/2017 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 8/22/2016 | 8/24/2016 | 8/31/2016 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 5/20/2016 | 5/24/2016 | 5/31/2016 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 2/18/2016 | 2/22/2016 | 2/29/2016 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 1/21/2016 | 11/23/2016 | 11/30/2016 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 11/19/2015 | 11/23/2015 | 11/30/2015 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 8/20/2015 | 8/24/2015 | 8/31/2015 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 5/20/2015 | 5/22/2015 | 5/29/2015 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 2/18/2015 | 2/20/2015 | 2/27/2015 | $0.44 | $0.00 | $0.00 | $0.00 | $0.44 | ||

| 11/19/2014 | 11/21/2014 | 11/28/2014 | $0.44 | $0.30 | $0.05 | $0.12 | $0.02 | ||

| 8/20/2014 | 8/22/2014 | 8/29/2014 | $0.44 | $0.30 | $0.05 | $0.12 | $0.02 | ||

| 5/20/2014 | 5/22/2014 | 5/30/2014 | $0.44 | $0.30 | $0.05 | $0.12 | $0.02 | ||

| 2/19/2014 | 2/21/2014 | 2/28/2014 | $0.44 | $0.30 | $0.05 | $0.12 | $0.02 | ||

| 11/20/2013 | 11/22/2013 | 11/29/2013 | $0.44 | $0.41 | $0.06 | $0.02 | $0.01 | ||

| 8/21/2013 | 8/23/2013 | 9/03/2013 | $0.44 | $0.41 | $0.06 | $0.02 | $0.01 | ||

| 5/21/2013 | 5/23/2013 | 6/03/2013 | $0.44 | $0.41 | $0.06 | $0.02 | $0.01 | ||

| 2/19/2013 | 2/21/2013 | 3/01/2013 | $0.44 | $0.41 | $0.06 | $0.02 | $0.01 | ||

| 11/20/2012 | 11/23/2012 | 11/30/2012 | $0.44 | $0.39 | $0.09 | $0.00 | $0.05 | ||

| Total 2012 Distributions: | $19.80 | $5.23 | $2.58 | $0.53 | $14.04 | ||||

-

Box 1a: Ordinary dividends are taxed at ordinary income tax rates.

-

Box 1b: Qualified dividends are taxed at capital gain tax rates if the stockholder meets holding period requirements.

-

Box 3: Nondividend distributions are nontaxable and considered return of capital.

For stockholders who participated in the company sponsored dividend reinvestment plan, the tax basis of shares acquired is the greater of the purchase price or the market close price on the payment date.

Report of Organizational Actions Affecting Basis of Securities

Effective January 1, 2012, issuers of regulated investment company securities must complete Form 8937 to report organizational actions, including nontaxable distributions, that affect the basis of the securities involved in the organizational action. The information contained below is intended to satisfy the requirements of public reporting under section 1.6045B-1(a)(3) and (b)(4) of the Treasury Regulations.

Nothing contained herein should be construed as tax advice; consult your tax advisor for more information. Furthermore, you may not rely upon any information herein for the purpose of avoiding any penalties that may be imposed under the Internal Revenue Code.